- How does exponential growth work, and how is it related to credit card debt?

Exponential growth is the way credit card companies charge their customers who do not completely pay off what they owe each month. There are two different ways credit card companies charge you depending on how much you pay off from the amount you owe. First, we will discuss what happens if you do not pay anything off of your credit card.

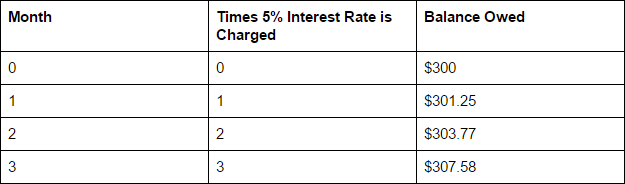

For the first month, the entire amount you owe is multiplied by an interest rate. When nothing is paid off, the amount of times that the interest rate is multiplied by the amount you owe increases. For instance, if you owe $300 the first month with an interest rate of 5% and you pay nothing off, you’ll owe $301.25 the second month because the interest rate is charged once. Then, if you still don’t pay off the $301.25 in the second month, the 5% interest rate is charged twice and you end up owing $303.77. This exponential growth continues on until the balance is completely paid off. The table below models this situation:

For the first month, the entire amount you owe is multiplied by an interest rate. When nothing is paid off, the amount of times that the interest rate is multiplied by the amount you owe increases. For instance, if you owe $300 the first month with an interest rate of 5% and you pay nothing off, you’ll owe $301.25 the second month because the interest rate is charged once. Then, if you still don’t pay off the $301.25 in the second month, the 5% interest rate is charged twice and you end up owing $303.77. This exponential growth continues on until the balance is completely paid off. The table below models this situation:

Now, let’s apply this concept to our three credit cards and interest rates.

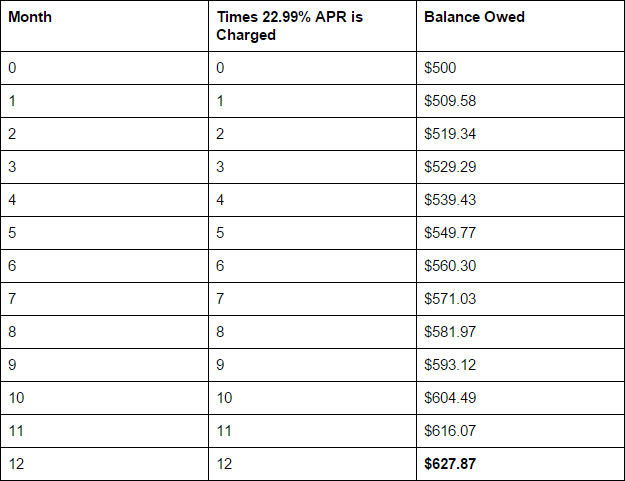

Our three example credit cards are Card A: Citi Double Cash, Card B: Chase Slate, and Card C: BankAmericard Travel Rewards Credit Card. Let’s start out with Card A. The penalty APR for this card is 29.99% which is charged when you miss a payment. The table below shows what happens if you do not pay off an initial amount of $500 spent on Card A for one year. Let’s assume you spend $500 the first month. Then, you continue to skip your payments for an entire year. At first, it doesn’t seem like much more is adding to your balance. But after a while it begins to add up, and at the end of the year you owe a whopping $627.87!!! That is $127 more than what you initially spent!

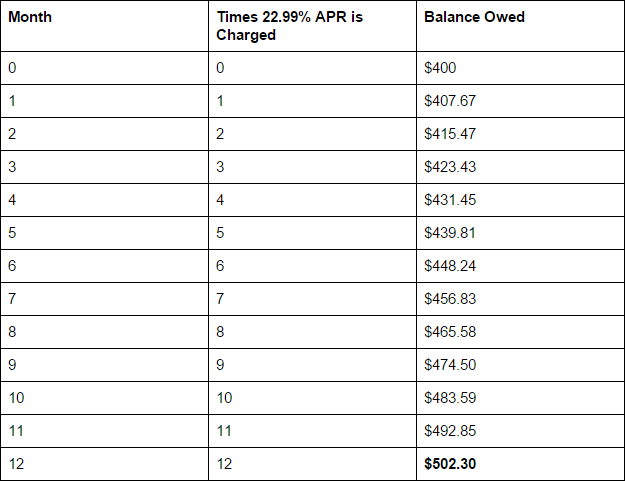

The table below exemplifies what happens if the same concept is applied to Card B with an initial amount of $400. After only one year, the balance owed ends up being $502.30! Yet again, there is more than a $100 jump through the year from what was initially spent!

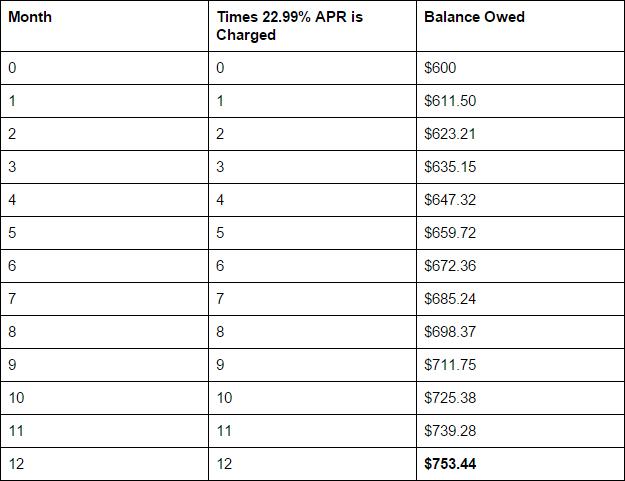

The table below exemplifies what happens if the same concept is applied to Card C with an initial amount of $600. The balance owed after only one year goes all the way up to $753.44!!! That’s more than a $150 increase! As you can see, the more the initial amount is, the more you’ll end up owing at the end of the year after making no payments.

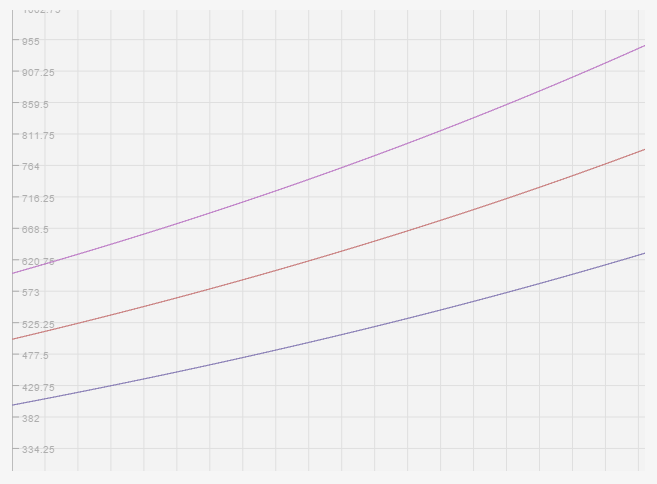

The graph below shows the same information of the exponential growth from the three credit cards shown above. The red line represents Credit Card A, The blue line represents Credit Card B, and the green line represents Credit Card C.

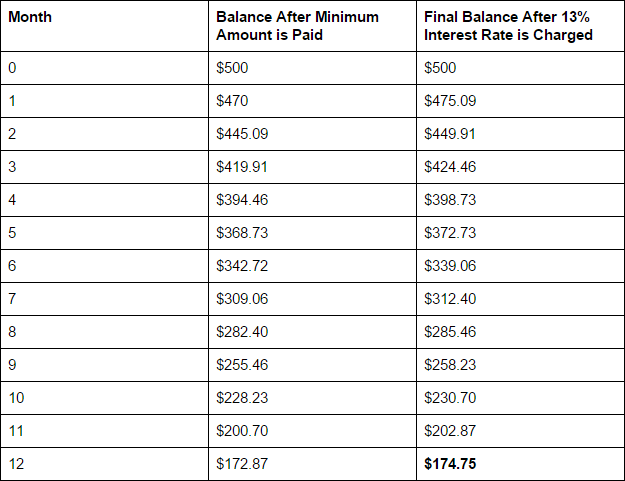

Now that we’ve explained what happens when you pay nothing off of our three example credit cards, we will discuss what happens if you pay off the minimum amount each month. Cards usually have a minimum payment amount that you must pay off in order to not be charged the penalty APR. Since all three credit cards have a wide range of interest rates between 12.99%-22.99%, let’s assume the interest rate being charged is 13%. The way credit card companies calculate the amount you owe is they subtract the amount you paid off and then they multiply the rest by the interest rate. The table below shows this situation with an initial amount of $500 spent on Card A and a minimum payment amount of $30 each month. At first, paying off the minimum amount seems like a good idea because you’ll just pay off a little at a time until your initial amount is paid off. However, as you can see, the amount you owe goes back up after the interest rate is charged so you’ll be paying more and much longer if you were to just pay it off in full. After an entire year of paying off the minimum amount each month, you still end up owing $174.75!

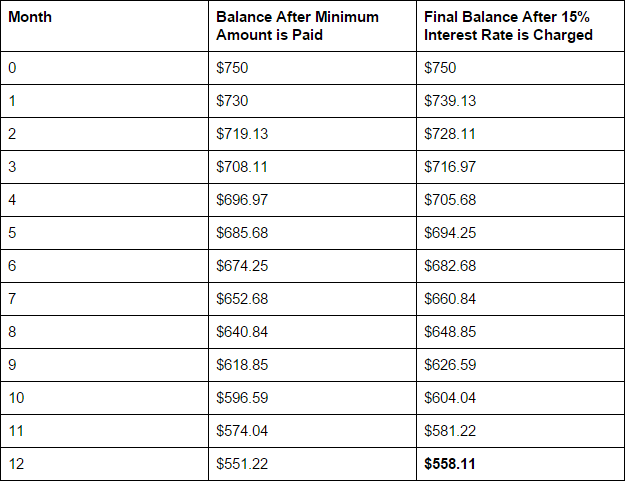

Let’s apply this same situation to a different credit card. Card B also has an interest rate between 12.99%-22.99%. For demonstrative purposes, we will set the interest rate at 15% and the minimum payment amount at $20 per month. The table below models the balance owed after one year with an initial amount of $750. After an entire year of making payments, you still owe $558.11! You went an entire year and barely paid off anything.

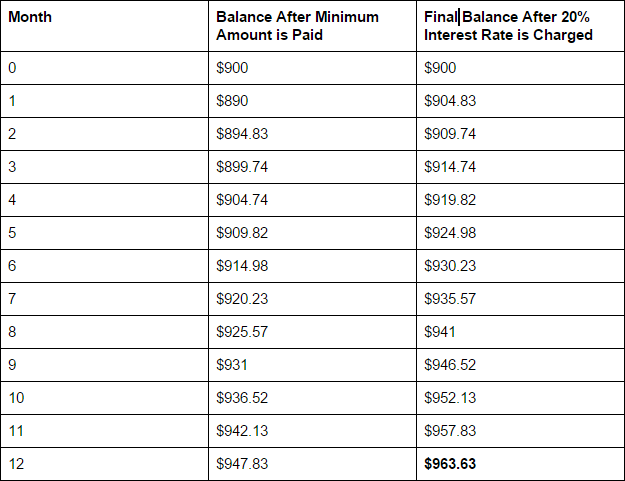

Finally, we will use this same concept with our last credit card. Card C has an interest rate range of 14.99%-22.99%. For our example, we will use an interest rate of 20% with an initial amount of $900. After an entire year of making minimum payments of $10, you still owe a whopping $963.63! Despite the minimum monthly payments you are making, that is even more than what you originally owed! Therefore, no matter how long you made minimum payments, you would never pay it off. You’d only end up owing much more money than what you started with. Therefore, the only beneficial alternative when obtaining a credit card is paying your monthly balance off in full.